Sunday Spectacle CXCVIII

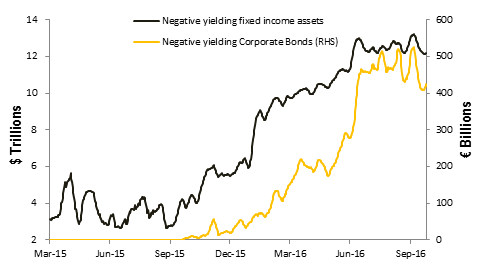

European Central Bankers Run Amok? I was in the deflation camp for a long time but even then, I never imagined yields would be negative. Amazing that even near-junk (BBB-rated) corporate bonds have negative yields! The data below is for Europe but similar situations are present in a few other regions (such as Japan). (source: Bank of America Merrill Lynch, via " These Are the Charts That Scare Wall Street ," Bloomberg.com, Oct 27 2016) (source: Bank of America Merrill Lynch, via " Bank of America: Here's One Way the ECB's Bond Buying Could Come to an End ," Bloomberg.com, Sep 8 2016)