Quick Thought On Ambac: Losses Shifting to HELOCs and CESes

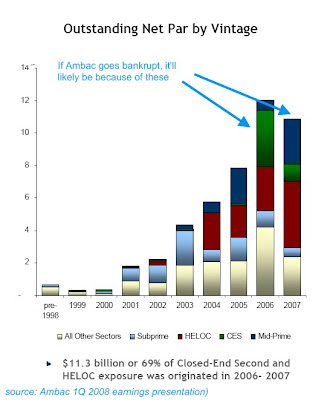

Looked deeper into the Ambac results and, although the losses are dissapointing and large, what is happening is not as surprising as it may seem. This isn't any consolation for any shareholder but here is how I see things. What is happening is that losses are "shifting" to HELOCs and CESes (for those not familiar, HELOC stands for home equity line of credit (basically people withdraw money by pledging their house); and CES stands for closed-end second lien (a mortgage backed by a subordinated claim on the house). This is not to say that CDOs aren't taking losses but the "surprisingly" large losses are showing up in HELOCs and CESes. This actually shouldn't be a surprise but given the magnitude of the numbers involved, it will shock anyone. Even some of the shorts are surprised by the large losses being posted. There are essentially two areas that can bankrupt the monolines: CDO-squareds and HELOCs/CESes. Depending on the insurance underwriting quality, ...