Toronto Housing Performance

The value investing mantra of buying an asset at low (undervalued) prices apply to housing as much as to stocks. The following excerpt from a Toronto Star analysis shows the performance of housing over various points of purchase over the last few decades.

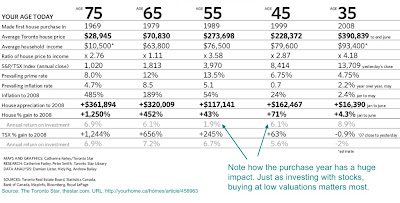

The table includes various statistics, including prime rate (interest rate charged to prime borrowers), inflation, house price to income ratio, and TSX (stock) return. A user comment to the story mentions that the stock market return seems to be price return only (so you should add roughly 3% to 5% to account for dividends.)

One of the points that stands out, not surprisingly, is how the returns on the house depend on the time period of purchase. For example, if you bought the house in 1989, your return was roughly 1.9% per year, whereas if you bought it in 1979 or 1999, you made 6.1% per year. Housing peaked somewhere near 1990 and it collapsed after the recession in 1990 so buying in the late 80's wasn't exactly a great idea (assuming you were buying the house to make money and not to live in it.)

Ratio of housing price to income was also relatively high (3.58x) in 1989 (versus less than 3x in prior and subsequent period.) The ratio also looks really high today (4.18x) so it is possible that housing will underperform or even decline over the short to medium term. However, the possibility of weak housing performance in the future is not certain for Toronto. Even though the house price to income ratio is high, prime rates are low, so mortage costs are likely to be much lower. Furthermore, housing is heavily dependent on population growth. Toronto has fairly high population growth, mostly due to immigration, so demand may be higher than in some of the prior periods. Yet, one shouldn't blindly rely on immigration to support housing because a lot of immigrants don't have enough money and the prices may out of reach.

One of the points I, as well as many analysts, have made is the possibility of stocks being under pressure due to higher inflation and interest rates in the future. The table illustrates clearly how present day interest rates are quiet low from a historical point of view. The 60's, 70's, and 80's had prime rates above 8% whereas it is 4.75% right now (I will note, however, that interest rates were lower in the 30's to 50's). Inflation and interest rates have been quite low in the last two decades due to globalization (particularly labour wage arbitrage) and rapid advances in technology (technology is inherently a deflationary force.) Some of those forces may be weakening and won't have as big of a downward pressure on inflation in the future. I am not in the inflation camp and don't see it being very high in the future. Some people expect interest rates to be much higher but I am not certain of that. All I am certain of is that interest rates (and inflation) will be higher than now (since it has been so low in the last few decades.) The question on whether it will get out of control remains to be seen.

The table includes various statistics, including prime rate (interest rate charged to prime borrowers), inflation, house price to income ratio, and TSX (stock) return. A user comment to the story mentions that the stock market return seems to be price return only (so you should add roughly 3% to 5% to account for dividends.)

One of the points that stands out, not surprisingly, is how the returns on the house depend on the time period of purchase. For example, if you bought the house in 1989, your return was roughly 1.9% per year, whereas if you bought it in 1979 or 1999, you made 6.1% per year. Housing peaked somewhere near 1990 and it collapsed after the recession in 1990 so buying in the late 80's wasn't exactly a great idea (assuming you were buying the house to make money and not to live in it.)

Ratio of housing price to income was also relatively high (3.58x) in 1989 (versus less than 3x in prior and subsequent period.) The ratio also looks really high today (4.18x) so it is possible that housing will underperform or even decline over the short to medium term. However, the possibility of weak housing performance in the future is not certain for Toronto. Even though the house price to income ratio is high, prime rates are low, so mortage costs are likely to be much lower. Furthermore, housing is heavily dependent on population growth. Toronto has fairly high population growth, mostly due to immigration, so demand may be higher than in some of the prior periods. Yet, one shouldn't blindly rely on immigration to support housing because a lot of immigrants don't have enough money and the prices may out of reach.

One of the points I, as well as many analysts, have made is the possibility of stocks being under pressure due to higher inflation and interest rates in the future. The table illustrates clearly how present day interest rates are quiet low from a historical point of view. The 60's, 70's, and 80's had prime rates above 8% whereas it is 4.75% right now (I will note, however, that interest rates were lower in the 30's to 50's). Inflation and interest rates have been quite low in the last two decades due to globalization (particularly labour wage arbitrage) and rapid advances in technology (technology is inherently a deflationary force.) Some of those forces may be weakening and won't have as big of a downward pressure on inflation in the future. I am not in the inflation camp and don't see it being very high in the future. Some people expect interest rates to be much higher but I am not certain of that. All I am certain of is that interest rates (and inflation) will be higher than now (since it has been so low in the last few decades.) The question on whether it will get out of control remains to be seen.

Indeed, investing in RE is a good choice, if you have the money and the right spirit, to know when and how to sell. The numbers look nice, but don`t forget that right now the prices are going down and it`s not a good time to sell to make money. But who knows the future, right? As of now, it is a good time to buy. In a few years the cycle will repeat and the time to sell will come. Right now especially investment in Toronto condos is looking bright. They are being built so fast, and prices are reasonable, that even with an unsteady population growth, they will be in high demand. Especially in Toronto, where it is quite unlikely to see development in detached houses in the future.

ReplyDeleteAll in all, if you`re an unexperienced investor, try the stocks first.

Elli