Timely Look at Gold: Still High Correlation to Broad Markets

(UPDATE near the end)

I tend to follow the gold market on and off, although I'm not really a goldbug and not really sold on its long-term merits. I sold off my only gold holding for no gain shortly after buying it and have missed the gold rally completely.

For what it's worth, the gold holding that I sold (and incidentally led to me missing the gold rally), Harmony (HMY), is not doing so well it seems. The stock is back near the levels I bought it at, while the gold market is rallying sharply. I still don't think I made a mistake in selling because my thesis for investing in gold did not materialize as you will see below (i.e. gold is still tracking the broad markets, albeit with a higher beta, so it can still collapse with the broad markets).

I think it's timely to look at the gold market right now for a few reasons. The broad markets have rallied sharply in the last couple of months, since the credit crisis. Practically everything has gone up but perhaps the biggest increase has been in the inflation trade (eg. cyclicals, commodities, gold, oil, commodity producing emerging markets, etc). It's still too early to say but if the last couple of days mean anything, it may be that the bear is starting to take a swipe here and there.

The main reason I sold out my gold investment just before gold took off is because I felt that gold was still correlated highly to the broad markets (I also did not buy the inflation argument so that's a second reason). I have little interest in gold or gold stocks if it is simply tracking the broad market with a higher beta. This may be some people's game but not mine. If gold is simply tracking the broad market, I find it more attractive to invest in broad market stocks who generally have better profitability.

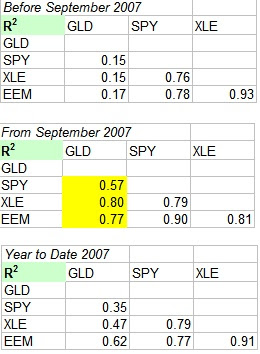

So the question in my eyes is whether gold is going to correct if the broad markets decline. To figure this out, I took some data from Yahoo Finance and calculated the correlations (you can do this in Excel with the built-in Analysis toolpak). The table below shows correlations between various ETFs (EEM=emerging markets; GLD=gold bullion; SPY=S&P 500; XLE=oil stocks).

I calculated the correlations (R-squared are shown) before September and after September. Before I forget I should note that the number of data points after September is quite small (only around 30 trading days) so the numbers aren't as statistically rigorous as the pre-September numbers (in fact I wouldn't use these numbers for anything serious and I just use it as a rough guide).

Unless there is something wrong with my calculation (or the source data), gold's correlation with broad market stocks has gone up significantly since the credit crisis. This is not good news for gold investors in my opinion. If the broad markets correct, I suspect gold is going to go down. Given that gold has a higher beta, it will plummet way more than broad market stocks.

All gold has done in the last month is simply go up when the broad market went up. There is nothing to indicate from my work that gold is moving independently of the broad markets. Some people seem to think that gold is moving on its own but I suspect they are being fooled by gold's high beta and various psychological reasons (such as some people placing higher significance when gold breaks even numbers like US$700).

None of this means that gold is or is not a good investment for you. If you want to play a declining US$ it is not a bad bet. But people like me would rather use something else to play a weakening dollar (eg. foreign stocks).

Gold and Stocks: No More Mortal Enemies--At Least For Now

UPDATE: Coincidentally, I ran into an article by Mark Hulbert at the New York Times on the relationship between gold and stocks. My comments were for the last two months but Mark Hulbert refers to a study which points out that gold and stocks have been moving together in the last few years. Historically gold has done well when inflation expectations were high, which generally also meant stocks did poorly; whereas gold and stocks have done well in the last few years while inflation expectations are low.

The theory given by the authors of the study is that rising incomes in developing countries has altered gold consumption. They expect this link to sever in the future. This is a view I share. In my opinion, people in developing countries like India consume a lot of gold because that is generally the best investment available (stocks and bonds are not readily accessible and most people distrust the government (particularly when it comes to currencies losing value all the time)). But I think as those markets develop, people will have greater access to stocks and bonds, and will finally realize that stocks are the #1 asset class. The governments in those countries have also significantly improved their economics, with more stable currencies (in fact the Indian Rupee has been rising lately).

I think all of this means that gold isn't what it was in the 70's. A lot of goldbugs invest as if massive inflation is around the corner but they may be in for a shock. The declining house prices alone should cause massive disinflation or deflation (typically, declining real estate causes huge downward forces on inflation).

(While on the topic of gold moving together with stocks, I suspect another reason, a minor one, is due to hedge funds putting on pair trades with gold. I'm sure that investors have funnelled a lot of money into gold to hedge their trades. I have no proof of any of this and most of the happenings in the hedge fund world is murky and happens in the dark.)

I tend to follow the gold market on and off, although I'm not really a goldbug and not really sold on its long-term merits. I sold off my only gold holding for no gain shortly after buying it and have missed the gold rally completely.

For what it's worth, the gold holding that I sold (and incidentally led to me missing the gold rally), Harmony (HMY), is not doing so well it seems. The stock is back near the levels I bought it at, while the gold market is rallying sharply. I still don't think I made a mistake in selling because my thesis for investing in gold did not materialize as you will see below (i.e. gold is still tracking the broad markets, albeit with a higher beta, so it can still collapse with the broad markets).

I think it's timely to look at the gold market right now for a few reasons. The broad markets have rallied sharply in the last couple of months, since the credit crisis. Practically everything has gone up but perhaps the biggest increase has been in the inflation trade (eg. cyclicals, commodities, gold, oil, commodity producing emerging markets, etc). It's still too early to say but if the last couple of days mean anything, it may be that the bear is starting to take a swipe here and there.

The main reason I sold out my gold investment just before gold took off is because I felt that gold was still correlated highly to the broad markets (I also did not buy the inflation argument so that's a second reason). I have little interest in gold or gold stocks if it is simply tracking the broad market with a higher beta. This may be some people's game but not mine. If gold is simply tracking the broad market, I find it more attractive to invest in broad market stocks who generally have better profitability.

So the question in my eyes is whether gold is going to correct if the broad markets decline. To figure this out, I took some data from Yahoo Finance and calculated the correlations (you can do this in Excel with the built-in Analysis toolpak). The table below shows correlations between various ETFs (EEM=emerging markets; GLD=gold bullion; SPY=S&P 500; XLE=oil stocks).

I calculated the correlations (R-squared are shown) before September and after September. Before I forget I should note that the number of data points after September is quite small (only around 30 trading days) so the numbers aren't as statistically rigorous as the pre-September numbers (in fact I wouldn't use these numbers for anything serious and I just use it as a rough guide).

Unless there is something wrong with my calculation (or the source data), gold's correlation with broad market stocks has gone up significantly since the credit crisis. This is not good news for gold investors in my opinion. If the broad markets correct, I suspect gold is going to go down. Given that gold has a higher beta, it will plummet way more than broad market stocks.

All gold has done in the last month is simply go up when the broad market went up. There is nothing to indicate from my work that gold is moving independently of the broad markets. Some people seem to think that gold is moving on its own but I suspect they are being fooled by gold's high beta and various psychological reasons (such as some people placing higher significance when gold breaks even numbers like US$700).

None of this means that gold is or is not a good investment for you. If you want to play a declining US$ it is not a bad bet. But people like me would rather use something else to play a weakening dollar (eg. foreign stocks).

Gold and Stocks: No More Mortal Enemies--At Least For Now

UPDATE: Coincidentally, I ran into an article by Mark Hulbert at the New York Times on the relationship between gold and stocks. My comments were for the last two months but Mark Hulbert refers to a study which points out that gold and stocks have been moving together in the last few years. Historically gold has done well when inflation expectations were high, which generally also meant stocks did poorly; whereas gold and stocks have done well in the last few years while inflation expectations are low.

The theory given by the authors of the study is that rising incomes in developing countries has altered gold consumption. They expect this link to sever in the future. This is a view I share. In my opinion, people in developing countries like India consume a lot of gold because that is generally the best investment available (stocks and bonds are not readily accessible and most people distrust the government (particularly when it comes to currencies losing value all the time)). But I think as those markets develop, people will have greater access to stocks and bonds, and will finally realize that stocks are the #1 asset class. The governments in those countries have also significantly improved their economics, with more stable currencies (in fact the Indian Rupee has been rising lately).

I think all of this means that gold isn't what it was in the 70's. A lot of goldbugs invest as if massive inflation is around the corner but they may be in for a shock. The declining house prices alone should cause massive disinflation or deflation (typically, declining real estate causes huge downward forces on inflation).

(While on the topic of gold moving together with stocks, I suspect another reason, a minor one, is due to hedge funds putting on pair trades with gold. I'm sure that investors have funnelled a lot of money into gold to hedge their trades. I have no proof of any of this and most of the happenings in the hedge fund world is murky and happens in the dark.)

The government is printing money so fast that even cash isn’t a safe bet any more. And even though gold has slumped during this crisis, the long-term outlook for gold investing remains attractive. Once institutional investors stop dumping gold holdings and the US dollar rally stalls, gold will zoom back up to $1,000 an ounce and beyond.

ReplyDelete