Quick Thought On Ambac: Losses Shifting to HELOCs and CESes

Looked deeper into the Ambac results and, although the losses are dissapointing and large, what is happening is not as surprising as it may seem. This isn't any consolation for any shareholder but here is how I see things.

What is happening is that losses are "shifting" to HELOCs and CESes (for those not familiar, HELOC stands for home equity line of credit (basically people withdraw money by pledging their house); and CES stands for closed-end second lien (a mortgage backed by a subordinated claim on the house). This is not to say that CDOs aren't taking losses but the "surprisingly" large losses are showing up in HELOCs and CESes. This actually shouldn't be a surprise but given the magnitude of the numbers involved, it will shock anyone. Even some of the shorts are surprised by the large losses being posted.

There are essentially two areas that can bankrupt the monolines: CDO-squareds and HELOCs/CESes. Depending on the insurance underwriting quality, there will be losses elsewhere as well but losses in those areas may be contained. The CDO-squareds are lethal because many of them have underlying assets that are mezzanine CDOs, and any mortgage payments will accrue, instead, to the senior tranches. It looks like Ambac has accounted for most of the potential CDO-squared losses.

The HELOCs and CESes can also result in massive losses because, again, mortgage payments will accrue to the first-lien and other obligations first. Unfortunately for Ambac--and MBIA as well--the HELOC and CES exposure is massive and has no seniority rights or other legal protections.

Here is where Ambac stands (pulled from their presentation):

Direct RMBS ($46.7 billion)

– Closed-End Seconds $5.0 billion

– HELOC: $11.4 billion <--- this is a scary number

– Mid-Prime (Alt A): $6.5 billion

– Sub-Prime: $8.1 billion

CDO of ABS (>25% MBS) portfolio ($32 billion)

– High-Grade CDO of ABS: $26.0 billion

– Mezzanine CDO of ABS: $0.5 billion

– CDO of CDOs: $2.5 billion

– Includes commitment to provide a financial guarantee on CDOs: $2.9 billion

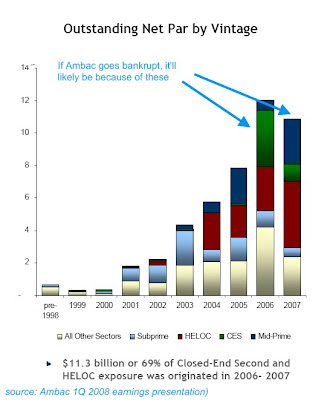

The HELOC is a scary-looking number and was mostly originated in 2006 and 2007--precisely the worst years to be insuring any mortgage!!! Here are some charts showing the HELOC and CES insured assets by vintages and ratings:

MBIA has an even worse HELOC exposure (although I'm not sure about their underwriting skills) and that is one of the reasons it posts large losses under the rating agency tests. If it weren't for the HELOCs and CESes, MBIA would be far better investment than Ambac (Ambac is heavily involved in CDOs, which are more opaque and complicated than direct RMBS.)

It'll be quite ironic if Ambac collapses, not because of its CDO exposure, which everyone thinks is the worst invention ever, but because of its really dumb strategy of insuring HELOC and CES.

What is happening is that losses are "shifting" to HELOCs and CESes (for those not familiar, HELOC stands for home equity line of credit (basically people withdraw money by pledging their house); and CES stands for closed-end second lien (a mortgage backed by a subordinated claim on the house). This is not to say that CDOs aren't taking losses but the "surprisingly" large losses are showing up in HELOCs and CESes. This actually shouldn't be a surprise but given the magnitude of the numbers involved, it will shock anyone. Even some of the shorts are surprised by the large losses being posted.

There are essentially two areas that can bankrupt the monolines: CDO-squareds and HELOCs/CESes. Depending on the insurance underwriting quality, there will be losses elsewhere as well but losses in those areas may be contained. The CDO-squareds are lethal because many of them have underlying assets that are mezzanine CDOs, and any mortgage payments will accrue, instead, to the senior tranches. It looks like Ambac has accounted for most of the potential CDO-squared losses.

The HELOCs and CESes can also result in massive losses because, again, mortgage payments will accrue to the first-lien and other obligations first. Unfortunately for Ambac--and MBIA as well--the HELOC and CES exposure is massive and has no seniority rights or other legal protections.

Here is where Ambac stands (pulled from their presentation):

Direct RMBS ($46.7 billion)

– Closed-End Seconds $5.0 billion

– HELOC: $11.4 billion <--- this is a scary number

– Mid-Prime (Alt A): $6.5 billion

– Sub-Prime: $8.1 billion

CDO of ABS (>25% MBS) portfolio ($32 billion)

– High-Grade CDO of ABS: $26.0 billion

– Mezzanine CDO of ABS: $0.5 billion

– CDO of CDOs: $2.5 billion

– Includes commitment to provide a financial guarantee on CDOs: $2.9 billion

The HELOC is a scary-looking number and was mostly originated in 2006 and 2007--precisely the worst years to be insuring any mortgage!!! Here are some charts showing the HELOC and CES insured assets by vintages and ratings:

MBIA has an even worse HELOC exposure (although I'm not sure about their underwriting skills) and that is one of the reasons it posts large losses under the rating agency tests. If it weren't for the HELOCs and CESes, MBIA would be far better investment than Ambac (Ambac is heavily involved in CDOs, which are more opaque and complicated than direct RMBS.)

It'll be quite ironic if Ambac collapses, not because of its CDO exposure, which everyone thinks is the worst invention ever, but because of its really dumb strategy of insuring HELOC and CES.

Comments

Post a Comment